Highland home owners among millions devastated by 'sickening' Bank of England interest rate hikes

Register for free to read more of the latest local news. It's easy and will only take a moment.

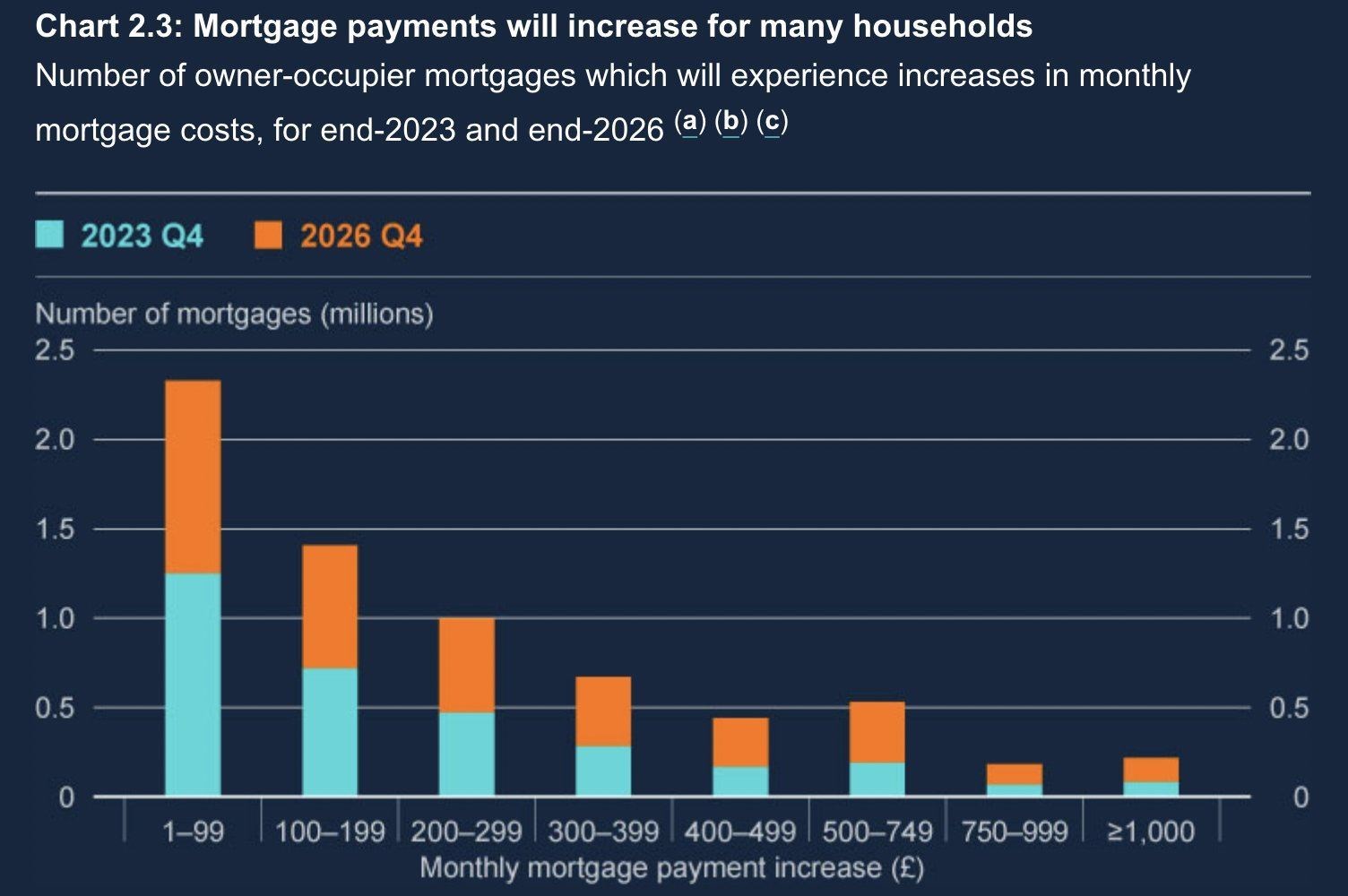

Around three million people with mortgages will be dramatically worse off by the end of 2026 due to interest rate hikes by the Bank of England – spelling disaster for prospective young Highland home owners.

The Bank, in its biannual Financial Stability Report yesterday, warned that for nearly one million households mortgage payments will rise by at least £500 a month and for more than two million it will rise between £200 and £499.

That means new home owners could end up having to pay more than 68 per cent of their take home wages a month for a mortgage based on the average wage, average house price and a six per cent interest rate.

John Burn-Murdoch, a columnist and chief data reporter at the Financial Times described the impact of the rates as "sickening" when considering them as a pay cut.

"The UK mortgage time bomb numbers are bad enough as they are, but they get really sickening when you think of them as an effective pay cut," he said.

"An increase of £500 in monthly payments (coming to 1m households by 2026) is £6000 per year, which equates to about a £10,000 pay cut."

The Governor of the Bank of England Andrew Bailey admitted: “It is going to have an impact clearly” but argued that due to “the resilience of the banking system” banks have the “ability to support customers and therefore manage the consequences of this.”

He added: “But there will be consequences from increased interest rates I’m afraid because that, from a monetary policy perspective, is why we have to do it.”

The rise in interest rates is already being felt in the Highlands as the council is finding it unaffordable to borrow to see itself through a financial crisis while under incredible cost pressures through inflation.

“The Bank just does not know what to do about that.”

Interest rates have risen from 0.1 per cent in December 2021 to five per cent in an effort by the bank to tackle inflation but Highland economist Tony Mackay argues the picture is more complex than the one being presented.

“The Bank of England’s inflation target is two per cent a year. However, the latest official statistics show it is currently at 7.8 per cent,” he said.

“Most forecasts show inflation falling to about four per cent by the end of 2023. However, it is very unlikely to fall to two per cent in the near future.

“The Bank of England (BoE) sets what is known as the base interest rate. Most interest rates, including mortgages and bank loans/savings interest are directly linked to that. So when the BoE increases the base rate so do the building societies, banks etc.

“The current base rate is five per cent. The bank has increased that 15 times in the last few years and is expected to increase it further to 5.5 per cent later this month.

“It will seem very strange to most people that the Bank of England’s main policy to try to reduce inflation is to increase their base rate. They believe that will reduce consumer spending and consequently inflation.

“However, there is no evidence of that happening in Scotland and the UK in recent years. To the contrary, many working people believe that if mortgage and bank interest rates increase, so too must their wages and salaries. The many current labour disputes are a testament to that belief.

“The obvious consequence at the present time is that if the Bank of England increases its base rate so will inflation increase. However, the Bank just does not know what to do about that.”

Prospective Highland home owners shut out of the market

That is incredibly bad news for young Highlanders and others struggling to get onto the housing ladder for the first time. First, many are already priced far out of the market by those buying up second homes and those who are buying to rent.

Hiking interest rates means that taking the average house price in the region of £212,748 and calculating a basic mortgage with a six per cent interest rate prospective homeowners would have to pay £1371 a month.

The average income in the Highlands £2012 a month (or £29,596 a year) so each month to pay bills, expenses, travel and food a single income household would be left with just £641.

Mr Mackay said: “The Highlands have been particularly badly hit by the economic recession in recent years because the various covid pandemics massively reduced the numbers of visitors. That badly affected many local shops, hotels, B&Bs and other businesses. The number of empty shops and other premises in Inverness shows that very clearly.

“There has been a revival in 2023 so far but I believe it will take a few years to recover.

“Another consequence of the covid pandemics was a huge fall in housebuilding in the region. That has left big shortages in both houses to buy and to rent. There also seems to have been a big switch by house owners to letting their properties as Air B&Bs etc rather than normal lets to local people.

“The announcement by the Bank of England states that average monthly mortgage payments will increase by about £500 a month. That will have serious implications for many Highland residents because income levels here are well below the Scottish and UK averages.

“I also fear that many people wanting to buy houses in the Highlands will not be able to do so because of the ongoing shortages and high prices. The local housing associations and the council need to take urgent action to increase the affordable housing supply in the region.”